The last of our four-part discussion of the common currency and its weaknesses.

Our trilogy on the euro currency is now in four parts (like Douglas Adams’ Hitchhiker’s Guide to the Galaxy) because we had to break off to discuss the Draft Withdrawal Agreement and other political developments. The previous parts dealt with the past, the present and the parallels with other monetary unions [1], we now turn to the consequences of the eurozone’s likely breakup.

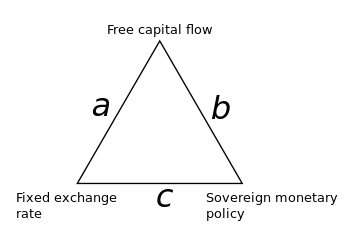

The essence of the problem is that no country can have a fixed exchange rate, free flow of capital and its own monetary policy; one of them has to adapt to economic stress. This is called the Impossible trinity or Trilemma. As Nobel Economics prize winner Paul Krugman says:

“… you can’t have it all: A country must pick two out of three. It can fix its exchange rate without emasculating its central bank, but only by maintaining controls on capital flows (like China today); it can leave capital movement free but retain monetary autonomy, but only by letting the exchange rate fluctuate (like Britain – or Canada); or it can choose to leave capital free and stabilize the currency, but only by abandoning any ability to adjust interest rates to fight inflation or recession (like … most of Europe).

If Italy, for example, lowered its interest rate to boost the growth of its stagnant economy, capital would seek better returns elsewhere. Outsiders wouldn’t invest in Italy if it imposed capital controls (in violation of one of the EU’s famous four freedoms) because they wouldn’t be able to get their money out again, and Italian capital that has already escaped (lots of it) won’t return either.

The EU Capital Requirements Directive (2013/36) requires all eurozone (EZ) governments’ debts to be rated at the same risk level, but Italian bonds pay higher returns than German bonds (perhaps the market knows something). Banks love high returns of course but zero-risk assets are great for its debt ratios because they don’t have to hedge against losses, so the banks are loaded up with EZ bonds. Meanwhile the European Central Bank (ECB) has become just about the only buyer but is meant to have stopped. What will happen to Italy’s borrowing rates? It can’t just print more banknotes – well, it sort of can but then so would others in similar trouble (see the mini-BOT [2]).

If you have money in the stock market and share prices fall it doesn’t actually matter unless you sell, then you “crystalise” the loss; stay invested and (hopefully) the market will recover and the loss never really happened. But if the market never recovers and eventually you need the money you’re in trouble. Money in the Target2 system is meant to ebb and flow but balance out in the end. It is so out of balance now that it can never rebalance itself except by massive default. Germany’s trade surplus actually finances others countries’ deficits but in some cases there is no hope of being repaid. Had this happened without Target2 there would already have been a major currency collapse; at least that would have ended it but instead of crisis and a resolution it just gets bigger. This cannot continue, Italian debt alone is fast approaching 2.5 trillion euros, and they’re not the only ones in trouble.

If you have money in the stock market and share prices fall it doesn’t actually matter unless you sell, then you “crystalise” the loss; stay invested and (hopefully) the market will recover and the loss never really happened. But if the market never recovers and eventually you need the money you’re in trouble. Money in the Target2 system is meant to ebb and flow but balance out in the end. It is so out of balance now that it can never rebalance itself except by massive default. Germany’s trade surplus actually finances others countries’ deficits but in some cases there is no hope of being repaid. Had this happened without Target2 there would already have been a major currency collapse; at least that would have ended it but instead of crisis and a resolution it just gets bigger. This cannot continue, Italian debt alone is fast approaching 2.5 trillion euros, and they’re not the only ones in trouble.

If the EZ shatters countries will adopt their own currencies with some depreciating massively. Debts governed by local law will be re-denominated with some big losses ensuing. However a great many contracts are written under English law – see why here [3] – sometimes even between parties wholly within the EZ. As Norvig [4] puts it:

“… a cross-border loan from a German bank to a Spanish corporate would typically be done under English law, and the contract would not be easy to re-denominate in a break-up scenario … In the extreme case of a full-blown break-up of the Eurozone, where the Euro would cease to exist, there would be an additional risk. In such a scenario, tens of trillions worth of obligations governed by English law and New York law would be stuck in redenomination-limbo. With no simple and remotely fair way to effect re-denomination in that scenario, we would be faced with prolonged legal proceedings. During this time, financial market participants would have no way to value some of the biggest exposures on their balance sheets. Most likely, courts would be overwhelmed, resulting in failure to quickly resolve payments on millions of financial contracts.”

Alternatively, with an agreed breakup it would help if a new currency-equivalent (ECU-2) were created, based on a basket of post-euro national currencies from the stronger eurozone economies. This could then be the basis for legally re-denominating the terms (the departing/weaker currencies having devalued).

Alternatively, with an agreed breakup it would help if a new currency-equivalent (ECU-2) were created, based on a basket of post-euro national currencies from the stronger eurozone economies. This could then be the basis for legally re-denominating the terms (the departing/weaker currencies having devalued).

Greece was small enough for Germany and the other, richer EZ nations to rescue but Italy is ten times bigger, it is beyond their means. Unless the eurozone effectively becomes a state with its own fiscal policy control (tax, spending, debt sharing and inter-regional subsidy) it must divide itself or shatter. There isn’t the popular will for the former solution, at least not in the states that would foot the bills, so a destructive or managed breakup is likely sooner or later. When that happens greedy banks and capitalists may take the blame for what the crazed politicians caused.

The politicians have been foolish, they have gambled that unity will prevail and so advance their project, but savers in Germany, Holland, Austria and Luxembourg won’t forgive them for their losses. When the crisis comes it will happen quickly so let’s hope there are secret plans in readiness. They must be secret or they could trigger a crash that harms us all, especially the UK which underpins so much of Europe’s financial system. A no-deal Brexit is an important but secondary problem for the world economy, it would help at least if we minimised our entanglement.

[1] State of the Euro The Future of the Euro-1 The Future of the Euro-2

[4] Rethinking the European Monetary Union (Wolfson Economics Prize, 2012)